Unlocking Your Dream Boat: Decoding the Credit Score Puzzle

Ready to captain your own vessel? Financing a boat is often a key step in making that dream a reality. But before you start picturing yourself at the helm, you'll need to navigate the waters of boat loan credit score requirements. Understanding these requirements is crucial for securing favorable loan terms and ultimately, getting the boat you want.

So, what credit score is needed for a boat loan? There isn't a single magic number, unfortunately. Lenders consider various factors, but your credit score is a major piece of the puzzle. It tells them how responsibly you've handled debt in the past and helps them assess the risk of lending to you. A higher score generally translates to better loan offers, including lower interest rates and more flexible repayment terms.

Similar to other loans, the required credit score for boat financing has evolved over time, reflecting economic conditions and lending practices. Historically, boat loans might have been easier to secure with a less-than-perfect credit history. However, lenders have become more stringent in recent years, placing greater emphasis on creditworthiness. Therefore, understanding the current landscape of boat loan credit requirements is essential for a smooth financing process.

The significance of a good credit score in securing a boat loan cannot be overstated. It impacts not only your ability to qualify for a loan but also the terms you'll receive. A lower credit score might mean a higher interest rate, a larger down payment, or even a loan denial. Conversely, a strong credit standing unlocks more favorable options, saving you money in the long run and making boat ownership more attainable.

One common misconception is that boat loans are only for those with exceptional credit. While a higher credit score certainly offers advantages, borrowers with average or even slightly below-average scores can still qualify. However, they might face less favorable terms. Understanding the minimum credit score requirements for different lenders and loan types is essential for setting realistic expectations and making informed decisions.

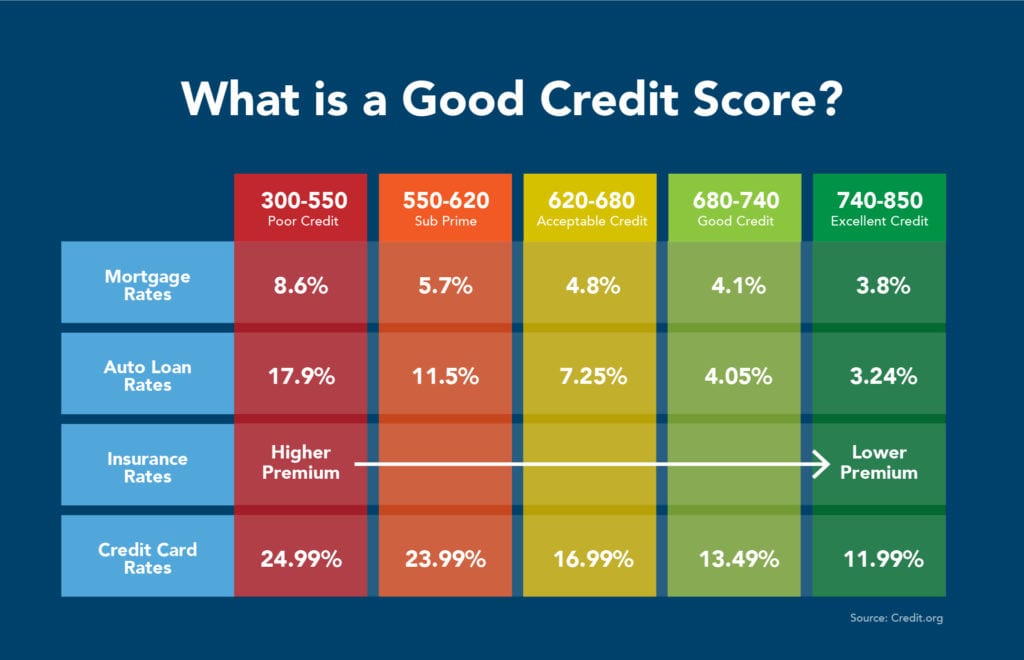

Generally, a credit score above 650 is considered good for a boat loan, increasing your chances of approval and competitive interest rates. Scores above 700 are even better, often unlocking the best loan offers. While some lenders may consider applicants with scores below 650, it becomes increasingly challenging, and you might encounter higher interest rates and stricter terms.

Benefits of a Good Credit Score for Boat Loans:

1. Lower Interest Rates: A strong credit score signals lower risk to lenders, leading to lower interest rates, which can translate to significant savings over the life of the loan.

2. Better Loan Terms: A good credit score can open doors to more favorable loan terms, including longer repayment periods and lower down payment requirements.

3. Increased Negotiating Power: A solid credit history provides more leverage when negotiating loan terms with lenders.

Action Plan for Improving Your Credit Score:

1. Check your credit report: Identify any errors or areas for improvement.

2. Pay bills on time: Payment history is a crucial factor in your credit score.

3. Reduce debt: Lowering your credit utilization ratio can significantly boost your score.

Advantages and Disadvantages of Focusing on Credit Score for Boat Loans

| Advantages | Disadvantages |

|---|---|

| Better loan terms | Can be time-consuming to improve |

| Increased approval chances | May limit loan options if score is low |

FAQs about Credit Scores and Boat Loans:

1. What is the minimum credit score needed? There's no universal minimum, but a score above 650 is generally recommended.

2. How can I improve my credit score? Pay bills on time, reduce debt, and check your credit report for errors.

3. Can I get a boat loan with bad credit? It's more challenging, but some lenders specialize in loans for borrowers with less-than-perfect credit.

4. Do different types of boats affect loan requirements? The type and price of the boat will influence the loan amount and potentially the lender's requirements.

5. What other factors do lenders consider? Income, debt-to-income ratio, and employment history.

6. How long does it take to get approved for a boat loan? The approval process can vary depending on the lender but typically takes a few days to a few weeks.

7. Should I get pre-approved for a loan? Pre-approval can give you a better understanding of the loan terms you qualify for and strengthen your negotiating position.

8. What are the different types of boat loans? Secured loans (using the boat as collateral) and unsecured loans.

Tips and Tricks: Shop around for the best loan rates, consider a larger down payment to reduce the loan amount, and be prepared to provide documentation of your income and financial history.

Understanding the importance of your credit score in securing a boat loan is paramount. A good credit score unlocks access to better loan terms, saving you money and making boat ownership more accessible. While the process might seem complex, by taking proactive steps to improve your credit and researching different lenders, you can navigate the waters of boat financing with confidence. By focusing on building a strong credit foundation, you put yourself in the captain's seat, ready to steer your dreams of boat ownership toward a successful voyage. Don't let credit score uncertainty hold you back. Start planning today and chart a course toward smooth sailing and financial peace of mind as you embark on your boat-buying journey.

Optum radiology syosset ny

Capture royal majesty learn how to draw queen elizabeth ii

Texas veggie time warp planting secrets revealed

.jpg)

{kind=link}